Malta SSC 2026: Social Security Contribution Rates, Classes and Employer Obligations

Malta social security contributions (SSC) for 2026 are split into two classes: Class 1 for employed persons and Class 2 for self-occupied and self-employed individuals. Class 1 contributions are paid equally by the employee and the employer at 10% of the basic weekly wage, subject to fixed minimum and maximum thresholds that vary by age and birth year. Class 2 contributions are paid solely by the individual at 15% of net annual income from the preceding year, subject to income-based bands.

SSC in Malta funds the national social security system administered by the Department of Social Security (DSS) under the Social Security Act (Cap. 318 of the Laws of Malta). The Malta Tax and Customs Administration (MTCA) — through the Office of the Commissioner for Revenue — publishes and administers the annual SSC rate tables. Both classes of contributions were revised upward with effect from 1 January 2026, reflecting a maximum increase of approximately 3% across all categories.

This guide covers the full Class 1 and Class 2 SSC rate tables for 2026, who pays each category, how contributions are calculated, the Maternity Leave Trust Fund levy, SSC for part-time workers and student workers, benefits funded by SSC, and employer payroll obligations.

What Are Social Security Contributions in Malta?

Social security contributions in Malta are mandatory payments made by employees, employers, and self-employed individuals to fund the national social security and pension system. SSC is also referred to as national insurance (NI) in Malta — both terms describe the same contribution obligation under the Social Security Act.

SSC is not a voluntary savings scheme. Every individual aged 16 or over who has not yet reached retirement age and is gainfully occupied in Malta — whether employed, self-occupied, or self-employed — is required to contribute.

Malta’s SSC system recognises 3 types of insurable employment:

- Employed persons — individuals working under a contract of service with an employer; pay Class 1 SSC

- Self-occupied persons — individuals earning income from a trade, business, profession, or vocation exceeding €910 per year; pay Class 2 SSC

- Self-employed persons — individuals earning income exclusively from passive sources such as rents, investments, and capital gains; pay Class 2 SSC (valid for pension purposes only)

There can only be one insurable employment at a time. Where a person holds more than one concurrent employment, the insurable employment is the one that provides the highest income.

Class 1 SSC 2026: Employed Persons

Class 1 social security contributions in Malta apply to all persons employed under a contract of service and are paid equally by the employee and the employer. The Class 1 rate structure for 2026 is divided into 6 categories — A through F — based on age, birth year, and weekly wage level.

Full Class 1 SSC Rate Table (2026)

| Category | Who It Covers | Employee Weekly Rate | Employer Weekly Rate |

|---|---|---|---|

| A | Persons under 18 years of age with basic weekly wage not exceeding €229.44 | €6.62 | €6.62 |

| B | Persons aged 18+ with basic weekly wage not exceeding €229.44 | €22.94 (or 10% of basic weekly wage if employee chooses) | €22.94 |

| C1 | Persons born on or before 31 December 1961 with weekly wage between €229.45 and €490.38 | 10% of basic weekly wage | 10% of basic weekly wage |

| C2 | Persons born on or after 1 January 1962 with weekly wage between €229.45 and €559.30 | 10% of basic weekly wage | 10% of basic weekly wage |

| D1 | Persons born on or before 31 December 1961 with weekly wage exceeding €490.39 | €45.19 (fixed) | €45.19 (fixed) |

| D2 | Persons born on or after 1 January 1962 with weekly wage exceeding €559.31 | €54.43 (fixed) | €54.43 (fixed) |

| E | Persons under 18 in full-time study under the Student-Worker Scheme | 10% of weekly remuneration, max €4.38 | 10% of weekly remuneration, max €4.38 |

| F | Persons aged 18+ in full-time study under the Student-Worker Scheme | 10% of weekly remuneration, max €7.94 | 10% of weekly remuneration, max €7.94 |

Source: Commissioner for Revenue (CfR), MTCA — 2026 Class 1 SSC rates

Key Points on the 2026 Class 1 Rate Structure

Category B — the minimum wage band: Workers aged 18 and over earning up to the national minimum wage of €229.44/week fall in Category B. Their fixed weekly SSC is €22.94 each for both employee and employer — equivalent to approximately 10% of the minimum wage. Category B employees may alternatively opt for 10% of their actual basic weekly wage if their wage is slightly below €229.44.

Category C — the 10% band: Workers earning between €229.45 and their applicable upper ceiling pay 10% of their exact basic weekly wage. This is the most common category for full-time employees in Malta earning between minimum wage and approximately €490–€560 per week (€25,500–€29,100 annually), depending on their birth year.

Category D — the capped maximum: Once weekly earnings exceed the upper ceiling for Category C, SSC is capped at a fixed maximum. Workers born before 1962 reach the maximum at earnings above €490.38/week, paying a fixed €45.19 each. Workers born from 1962 onward reach the ceiling at earnings above €559.30/week, paying a fixed €54.43 each. No additional SSC applies to earnings above these thresholds.

The birth year split matters: The 2026 rate structure uses 31 December 1961 as the dividing line between two different ceiling levels. This distinction has persisted in Maltese SSC law for several years as part of pension reform adjustments. Workers born from 1962 onward face a higher earnings ceiling before the fixed cap applies, meaning they pay 10% of a wider wage band than older workers.

Class 1 SSC: Weekly Ceilings and Maximum Contributions 2026

The Class 1 SSC ceiling determines the maximum weekly contribution payable regardless of how much the employee earns above the threshold. Once an employee’s basic weekly wage exceeds the ceiling, both employee and employer pay the fixed Category D amount — no further SSC is due on earnings above the ceiling.

| Birth Year | Weekly Earnings Ceiling | Maximum Weekly SSC (Each Side) | Maximum Annual SSC (Each Side) |

|---|---|---|---|

| Born on or before 31/12/1961 | €490.38 | €45.19 | ~€2,350 |

| Born on or after 01/01/1962 | €559.30 | €54.43 | ~€2,830 |

This ceiling structure makes SSC partially regressive at higher income levels. An employee earning €60,000 per year pays the same nominal SSC as an employee earning €35,000 (both in Category D), while a lower-earning employee in Category C pays 10% of their full weekly wage.

Maternity Leave Trust Fund Contributions 2026

In addition to standard SSC, employers and employees pay a Maternity Leave Trust Fund (MLTF) levy on top of the Class 1 social security contributions. This levy funds Malta’s maternity leave benefit payments.

The MLTF contribution rates for 2026 are applied alongside each SSC category and represent a small fixed or percentage addition to the weekly contribution. The rates are published annually by the MTCA alongside the main SSC tables and apply to both employed persons and their employers.

Maternity Leave Trust Fund levies continue to be applied on top of social security contributions at specified rates for 2026, adjusted in line with the broader SSC rate revisions.

Class 2 SSC 2026: Self-Occupied Persons

Class 2 social security contributions for self-occupied persons in Malta are based on the net annual profit or income earned during the year preceding the contribution payment year, not the current year’s income. A self-occupied person paying SSC in 2026 bases contributions on the net profit declared for the 2025 tax year.

Who Is a Self-Occupied Person?

A self-occupied person is any individual who earns income from a trade, business, profession, vocation, or any other economic activity exceeding €910 per year and who is not employed under a contract of service. Common examples include freelancers, sole traders, professionals in private practice, and business owners who work in their own enterprise.

Class 2 Self-Occupied contributions are valid for both pension entitlement and short-term benefit eligibility (including sickness and injury benefits), making them functionally equivalent to Class 1 for the purposes of contribution record-building.

Class 2 Self-Occupied Rate Structure (2026)

Class 2 self-occupied contributions are calculated on a weekly basis derived from annual net income bands. Rates for 2026 range from approximately €31.97 per week for lower income brackets to €83.89 per week for higher income brackets, based on the prior year’s net income.

A minimum weekly contribution of €36.18 applies: if the calculated contribution falls below this threshold, the individual may elect to pay the minimum, though contributing below the full rate may result in a reduced contributory benefit or pension entitlement. Full-time farmers qualify for a reduced rate on application.

Payment schedule: Self-occupied persons pay Class 2 SSC contributions every 4 months — in April, August, and December — to the Commissioner for Revenue. Contributions are not withheld at source by an employer; the individual is personally responsible for timely payment.

Part-time self-occupied option: Part-time self-occupied females, students under the age of 25, and pensioners whose earnings do not exceed the minimum income threshold for Class 2 Rate SA may opt for a reduced Class 2 Pro-rata rate of 15% of basic weekly income. Contributions paid at this reduced rate carry lesser proportional weight in the contribution record compared to full weekly contributions. Individuals wishing to pay at the pro-rata rate must apply to the MTCA Commissioner for Revenue before doing so.

Class 2 SSC 2026: Self-Employed Persons

Class 2 social security contributions for self-employed persons apply to individuals whose income derives exclusively from passive sources — rents, investments, capital gains, or other income not registered with Jobsplus as a gainful occupation.

The key distinction between self-occupied and self-employed SSC in Malta is the benefit scope:

| SSC Type | Income Source | Pension Entitlement | Short-Term Benefits |

|---|---|---|---|

| Class 2 — Self-Occupied | Trade, business, profession, vocation | ✅ Yes | ✅ Yes |

| Class 2 — Self-Employed | Rents, investments, capital gains | ✅ Yes | ❌ No |

Self-employed persons’ contributions are valid only for pension purposes. A self-employed individual cannot claim sickness benefit, injury benefit, or unemployment assistance based on Class 2 self-employed contributions alone.

The Department of Social Security records self-employed contributions as Class 3 in the Social Security Contribution Record Sheet, even though they are technically paid as Class 2 under the MTCA system.

Threshold: Class 2 contributions are payable by all individuals who derive income of more than €910 from an economic activity and who are not employed. Below this threshold, no SSC obligation arises.

SSC for Part-Time Employees (Class 1)

Part-time employees in Malta pay Class 1 SSC at the same percentage rate as full-time employees, with contributions calculated on actual basic weekly remuneration rather than a fixed minimum. Part-time workers whose weekly earnings fall below the Category B threshold pay 10% of their actual weekly remuneration.

Where a part-time employee earns a weekly wage proportionate to the minimum wage, the applicable SSC category is determined by their actual weekly rate of pay — not by annualised figures. A part-time worker earning €5.74/hour (the minimum hourly rate for 2026) for 20 hours per week earns €114.72/week and pays SSC on that amount.

Employers pay an equal contribution on the part-time employee’s actual weekly remuneration, following the same category structure as for full-time employees.

SSC for Student-Workers (Categories E and F)

Student-workers in Malta who are receiving remuneration through the Student-Worker Scheme — involving distinct work and study periods — pay SSC at 10% of their weekly remuneration, subject to maximum weekly caps.

The 2026 caps are:

- Category E (under 18): Maximum weekly SSC of €4.38 each for student and employer

- Category F (18 and over): Maximum weekly SSC of €7.94 each for student and employer

These capped rates recognise that student-workers are typically engaged on a part-time or scheme-specific basis and apply only to the Student-Worker Scheme and Extended Skills Training Schemes. Worker-Student Schemes — where the individual is primarily an employee pursuing studies — do not qualify for these capped rates and follow standard Category A or B rates.

Benefits Funded by SSC in Malta

Social security contributions in Malta fund 8 main categories of contributory benefits under the Social Security Act (Cap. 318):

- Retirement pension — contributory pension payable from retirement age (61–65 depending on year of birth)

- Sickness benefit — daily benefit for incapacity to work due to illness, funded by Class 1 and Class 2 Self-Occupied contributions

- Injury benefit — payable for work-related injury or industrial disease

- Unemployment benefit — contributory benefit for insured workers who become unemployed

- Marriage grant — one-off payment upon marriage for qualifying contributors

- Maternity benefit — funded through the Maternity Leave Trust Fund alongside SSC

- Children’s allowance — means-tested, linked to contribution record in certain cases

- Widows’/widowers’ pension — contributory survivor pension for qualifying spouses

The weight given to each week of contribution varies depending on the class and type of contribution paid. Class 1 contributions from employment carry full weight. Class 2 Pro-rata contributions for part-time self-occupied persons carry a lesser proportional weight, which can reduce the eventual benefit or pension entitlement.

Retirement age in Malta for 2026 is 65 for most workers born from 1962 onward, with earlier pension ages applying to those born before 1962 under a graduated transition schedule established by pension reform legislation.

How SSC Is Paid: Employer Obligations in Malta

Employers in Malta are responsible for deducting employee SSC from each payslip and remitting both the employee’s and employer’s SSC contributions to the MTCA monthly, through the Final Settlement System (FSS). SSC is not paid by the employee directly — the employer withholds and remits on the employee’s behalf.

Employers have 4 payroll obligations related to SSC each month:

- Calculate the applicable SSC category for each employee based on age, birth year, and basic weekly wage

- Deduct the employee SSC amount from the employee’s gross pay

- Add the employer SSC amount — the employer bears this cost on top of gross salary

- Remit both amounts to the Commissioner for Revenue by the end of each calendar month

Failure to correctly calculate, deduct, or remit SSC is a breach of the Social Security Act and the Employment and Industrial Relations Act (EIRA). The MTCA and the Department of Social Security jointly have powers to investigate and pursue employers for outstanding contributions, with interest and penalties applying to late payments.

Employers using payroll software in Malta — such as Shireburn Indigo or managed payroll services from firms such as PwC Malta or BDO Malta — update SSC rate tables at the start of each calendar year following the official MTCA rate publication.

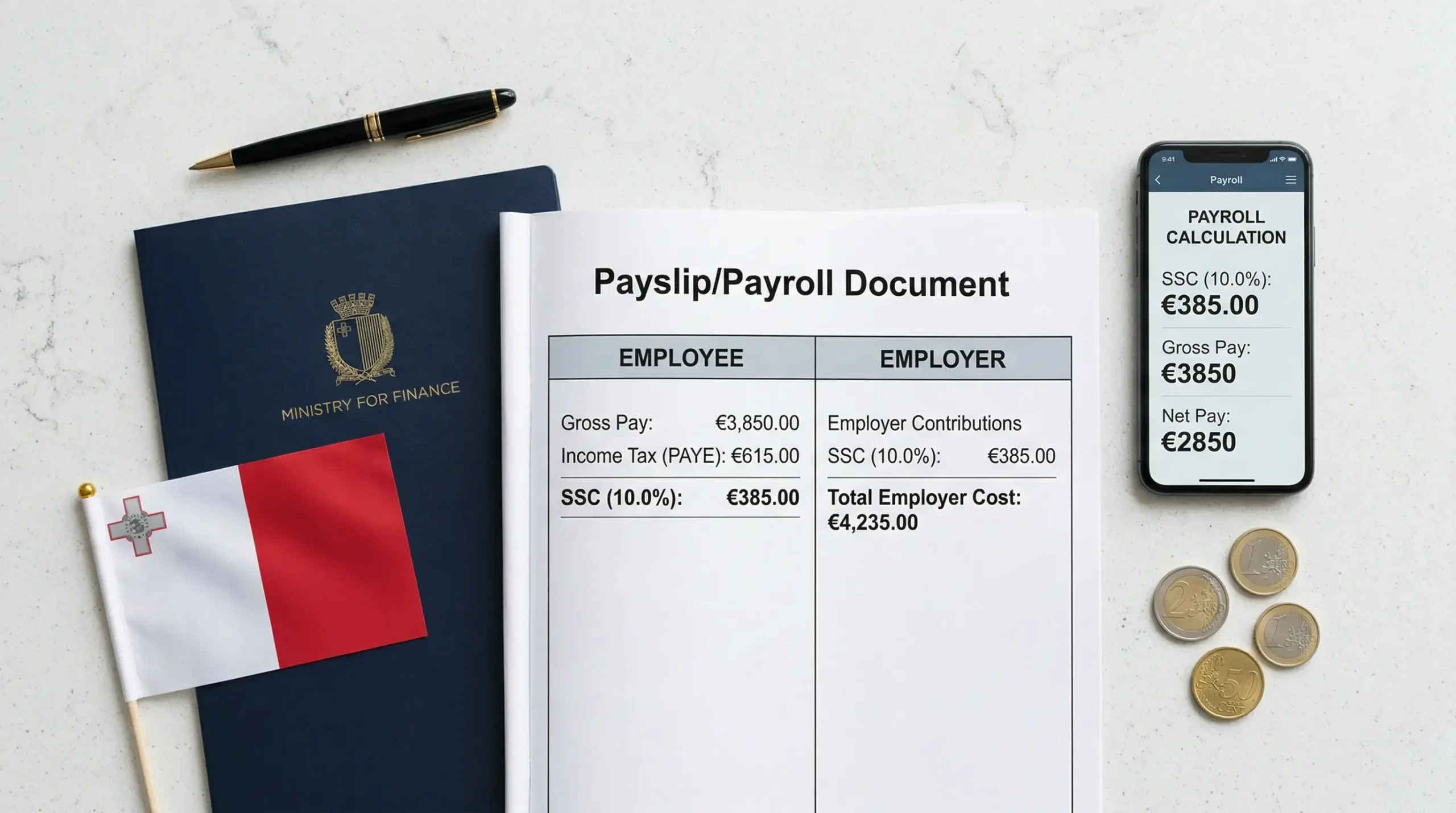

SSC and Gross-to-Net Salary: A Worked Example

For a full-time employee aged 30 (born 1996, i.e. Category C2 in 2026) earning a basic weekly wage of €400:

| Component | Calculation | Amount |

|---|---|---|

| Basic weekly gross | — | €400.00 |

| Employee SSC (10%) | €400 × 10% | €40.00 |

| Employer SSC (10%) | €400 × 10% | €40.00 |

| Combined SSC (both sides) | — | €80.00 |

| Annual employee SSC (×52) | €40 × 52 | €2,080.00 |

| Annual employer SSC (×52) | €40 × 52 | €2,080.00 |

| Annual combined SSC cost | — | €4,160.00 |

For the same employee, annual income tax on €400/week (€20,800/year) using the single rate table would be approximately €1,975. Combined, SSC plus income tax account for approximately €4,055 per year in direct deductions from gross pay — an effective total deduction rate of approximately 19.5% before any allowances.

The employer’s total cost is €400/week gross + €40/week employer SSC = €440/week (€22,880/year) to employ this individual, compared to the employee’s net take-home of approximately €340–€345/week after tax and SSC.

SSC for Persons Employed Abroad but Resident in Malta

Individuals who are employed under a contract of service outside Malta but who retain ordinary residence in Malta may request the Department of Social Security to pay Class 1 contributions instead of Class 2, under Article 13(1) of the Social Security Act (Cap. 318).

Where this request is granted, no SSC is payable by or on behalf of the employer. The individual pays both the employee and employer portions of Class 1 contributions, maintaining their contribution record and benefit eligibility in Malta despite working abroad.

For EU/EEA/Swiss crew employed on a Malta-flagged vessel or by a Maltese entity, EU Regulation 883/2004 requires contributions to the Maltese social security system. The 2026 SSC rates increased by a maximum of approximately 3% for these workers, with capped weekly rates applying based on working periods aboard the vessel.

Non-EU/EEA/Swiss residents working on a Malta-flagged vessel are not eligible to affiliate with Malta’s social security system and may instead remain affiliated with the social security system of their own country of residence.

2026 SSC Changes vs 2025

The 2026 SSC changes represent a moderate upward adjustment across all categories, designed to reflect nominal wage growth and preserve the real value of social security financing. The core rate structure — 10% of basic weekly wage for Class 1, 15% of net annual income for Class 2 — remains unchanged from prior years.

The 3 headline changes for 2026 are:

- Updated wage thresholds for Categories C and D — the weekly ceiling levels for the 10% band and the fixed maximum cap were revised upward in line with wage trends

- Revised fixed amounts for Categories A, B, D, and student-worker caps — all fixed euro amounts increased by approximately 3% from 2025 levels

- Updated Class 2 income bands — the annual net income thresholds determining which weekly Class 2 rate applies were adjusted upward for both self-occupied and self-employed persons

These adjustments were confirmed by the MTCA with effect from 1 January 2026, consistent with routine annual updates to the SSC schedule following the Malta Budget announcement.

Frequently Asked Questions: Malta SSC 2026

What is the SSC rate in Malta for employees in 2026?

The SSC rate for employees in Malta in 2026 is 10% of the basic weekly wage for most workers (Categories C1 and C2), subject to a fixed minimum for those earning at or below the minimum wage and a fixed maximum for those earning above the weekly ceiling. Both the employee and employer each pay 10% — making the combined SSC cost 20% of the basic weekly wage up to the applicable ceiling.

What is the difference between Class 1 and Class 2 SSC in Malta?

Class 1 SSC applies to employees working under a contract of service, while Class 2 SSC applies to self-occupied and self-employed individuals. Class 1 is split equally between employee and employer; Class 2 is paid entirely by the individual. Class 1 contributions fund pension entitlement and all short-term benefits. Class 2 self-occupied contributions fund both pension and short-term benefits; Class 2 self-employed contributions fund pension entitlement only.

How much SSC does an employer pay in Malta in 2026?

An employer in Malta pays SSC at an equal rate to the employee’s contribution for every worker on their payroll. For most employees in Category C2, this is 10% of the employee’s basic weekly wage up to the weekly ceiling of €559.30, capped at a maximum of €54.43 per week. For Category B (minimum wage workers aged 18+), the employer pays a fixed €22.94 per week. Employer SSC is an additional cost on top of gross salary and is remitted monthly to the Commissioner for Revenue.

When do self-employed individuals pay SSC in Malta?

Self-employed and self-occupied individuals in Malta pay Class 2 SSC contributions every 4 months — in April, August, and December — to the Commissioner for Revenue. The contribution amount is based on the net annual income declared for the year before the payment year, not the current year’s earnings. No employer withholds or remits SSC on behalf of a self-employed individual.

Does SSC in Malta affect pension entitlement?

Yes, SSC contributions in Malta directly determine pension entitlement. The number of weekly contributions paid throughout a working life forms the contribution record used to calculate the contributory retirement pension. Class 1 and Class 2 self-occupied contributions carry full weight per week. Class 2 self-employed contributions are valid for pension only. Class 2 Pro-rata contributions carry lesser proportional weight, potentially reducing the eventual pension amount. Individuals can request their contribution record from the Department of Social Security at any time.

What happens if an employer fails to pay SSC in Malta?

Employers who fail to correctly calculate, deduct, or remit SSC are in breach of the Social Security Act (Cap. 318) and face penalties, interest charges, and potential legal action from the MTCA and the Department of Social Security. Unpaid SSC can also impact the affected employee’s contribution record if the Department of Social Security is not notified of the employment. Employees have the right to verify their contribution record and report discrepancies directly to the Department of Social Security.

Conclusion

Malta’s social security contribution system for 2026 operates through two main classes: Class 1 at 10% of basic weekly wage for employed persons, split equally between employee and employer, and Class 2 at 15% of net annual income for self-occupied and self-employed individuals. Both classes were revised upward by approximately 3% effective 1 January 2026, following the annual Malta Budget process.

Class 1 SSC covers 6 categories — A through F — with fixed amounts for minimum wage workers and student-workers, a 10% rate for mid-range earners, and fixed weekly caps for higher earners that differ by birth year (€45.19/week for those born before 1962, €54.43/week for those born from 1962 onward). Class 2 rates are income-band driven and range from approximately €31.97 to €83.89 per week for self-occupied persons.

Employers bear the full administrative responsibility for Class 1 SSC — calculating the correct category, deducting the employee portion, contributing the equal employer portion, and remitting both to the Commissioner for Revenue monthly through the Final Settlement System (FSS). Self-occupied and self-employed individuals manage Class 2 payments independently on a 4-monthly schedule.

All SSC obligations in Malta are governed by the Social Security Act (Cap. 318 of the Laws of Malta), administered by the Malta Tax and Customs Administration (MTCA) and the Department of Social Security (DSS). The official annual rate tables are published on the MTCA website at cfr.gov.mt.